WHEN I PLACED MY GARY SULLIVAN ID on the counter of the pristine Columbia, South Carolina branch of Wachovia Bank in March 2005, I appeared to be just another clean-cut businessman sporting a Rolex in Dolce & Gabbana; conducting a routine bank transaction, removing some cash from one of my many accounts scattered throughout the city’s banks. In fact, I was the U.S. Secret Service’s most wanted fugitive, Matthew B. Cox, one of the most notorious, mortgage fraud con artists of all time; and I was doing what I did best, bilking the banks out of millions.

I’d removed half a million dollars in fraudulent loan proceeds over the last few weeks. So I wasn’t concerned when the bank teller gave me a strained smile and stepped into the back room to make a quick call “for approval.” It was standard Wachovia policy on new accounts. But I wasn’t worried, my credentials were perfect.

During the last three years, I’d swindled most of America’s biggest banks out of more than $15 million using fake and stolen identities, forgeries and my knowledge of the mortgage industry. I’d manipulated public records, all three credit bureaus, defeated the security procedures of six states’ department of motor vehicles and the U.S. State Department’s passport services. And I’d done it all while on federal probation or as a fugitive being sought by the FBI, the Secret Service and the U.S. Marshals.

I’d managed to stay one step ahead of the authorities for years, but today my luck was about to run out. I didn’t notice the two massive Richland County Sheriff’s deputies slip into the bank’s lobby while the teller counted out my withdrawal in crisp one hundred dollar bills. Nor was I aware the officers had crept up behind me, until one of them pulled my wrists behind my back and slapped a pair of stainless steel handcuffs on me.

My heart was pounding as the deputies escorted me through the crowd of shocked Wachovia customers into the bank manager’s office. We were then joined by an investigator from the Columbia Police Department. I was told that the head of Wachovia’s fraud department wanted me, Gary Sullivan, arrested for bank fraud.

I’d slipped through the authorities’ fingers on more than one occasion, but this time was different. This time they had me in handcuffs.

Over the last several months, I’d purchased two houses using the stolen identity of Gary Sullivan; filed forged Satisfactions of Mortgage with public records—cleaning the titles of all mortgage liens. I then borrowed $1.3 million in new mortgages against the homes, from separate banks, including Wachovia.

Posing as Sullivan, I was in the middle of removing the fraudulent funds when the deputies grabbed me. However, no one seemed to have made the connection that Sullivan was the fugitive Cox. After all, I had a State of South Carolina ID, a Federal Social Security Card and a Wachovia Visa—all valid, and all in Sullivan’s name.

When the investigator got the head of Wachovia’s fraud department on the phone he was adamant that Sullivan was running a multiple-mortgage scam. Although at the time, Wachovia’s “fraud guy” wasn’t quite sure how I’d managed to pull it off.

With the steel handcuffs digging into my wrists and Wachovia’s fraud guy screaming in the background, I somehow convinced the Columbia police investigator to release me.

“THE GUY WAS GOOD. Very good,” said Assistant U.S. Attorney Gale McKenzie, the lead prosecutor in my case, during an interview with The Atlanta Journal-Constitution. “Cox knew we were close at that point.” The number of victim banks, the amount of stolen identities used and the sophistication of the scheme itself, makes this case very unique. “Nothing deterred him … Stops by law enforcement didn’t.” Even after the Richland County Sheriff’s Office released me; “Cox didn’t run, he went to several more banks and emptied accounts.”

Then, just as I’d done in Tampa, Orlando, St. Petersburg, Tallahassee and Atlanta, I climbed into a luxury sports car—with a duffel bag full of cash—and vanished.

THE PRESS was calling me a “mastermind” and a “silver tongued liar,” but nothing in my early academic career foreshadowed that. At age six, I failed the second grade. After a battery of tests, I was diagnosed with a severe case of dyslexia and a genius IQ. Due to over-crowding in the Florida public school’s special needs classes, I was placed in the mentally handicapped program with students suffering from mild-to-severe retardation, Down’s Syndrome and Tay-Sach’s Disease—what my peers referred to as the “Mr. Potato Head classes with the droolers, riding the short bus.”

My mother, Margaret Cox, pled with the principal to find room in the correct program. “Matthew’s smart and talented,” she told him. “He doesn’t belong in those classes.” But there was nothing he could do.

Out of frustration, I began running away from school. I’d show up at my parents’ front door an hour later in tears. My father was an overbearing alcoholic who would go on week long, drunken binges and berate me for my shortcomings. I once asked my mother, “Why’d you stay married to Dad?” She told me, “He was a good provider.” That may have been true, but he never understood me.

I eventually ended up in a school for troubled, learning disabled kids, where, by some miracle, I obtained my high school diploma.

At the University of South Florida, I pursued a degree in Fine Arts, after being told by my career counselor that a degree in Business was “doubtful” due to the severity of my learning disability. With the exception of fraud, art was the only thing I’ve ever excelled at. After four years of sculpting, painting, graphic design and printmaking, I graduated summa cum laude. I remember my father commenting, “The best you can hope for with that degree is drawing caricatures of sweaty tourists at Disney World or paint portraits of aging trophy wives.” The worst thing about his comment was, he was right.

My college degree didn’t guarantee me a spot in corporate America. After several layoffs and downsizings, I ended up working construction jobs for slightly more than minimum wage. I was broke and demoralized. My girlfriend at the time was working for a sub-prime lender and she kept pushing me to give the mortgage industry a try. “You were absolutely made for this,” she used to say.

She was right. It came easily to me. Everything was computerized, and what little paperwork there was, the loan processors handled. However, I learned right away not everyone qualifies for a loan. A week before my first closing, the borrower’s Verification of Rent form indicated she’d been 30 days late on her rent. It was a deal killer. My qualified borrower was circling the bowl and taking my commission with her.

My manager actually handed me the bottle of White-Out and said, “Get rid of it.”

“That’s bank fraud,” I replied. At 27, I’d never broken the law. “Could I get in trouble?”

“If underwriting catches it, you could lose your job. But they won’t.” My finances were bleak, I was behind on everything. My credit cards were being declined, the repo man was looking for my vehicle and the bank was threatening to foreclose. I was within weeks of having to move into my parents’ spare room, where I’d have to hear my father boss around my mother and make comments about her “loser son.”

I snapped and whited out the late payment. A week later, the loan closed and I walked away with a commission check. It changed everything for me. I became emboldened by it. I started cutting and pasting together W-2’s, pay stubs and cancelled checks. Before long, all my clients were approved.

By the time I opened my own mortgage company, Consortium Financial Services in 1998, I was regularly altering documents for the dozen associates working underneath my brokerage license. Consortium was a bonanza of bank fraud. If you walked in that office with a pulse, you were getting a loan.

The FBI estimated over $40 million in fraudulent mortgages flowed through my brokerage business during my tenure; and we got caught all the time, by lenders like Wells Fargo, Countrywide and Union Planters Bank.

Pinnacle Bancorp once came across almost $2 million in fraudulent mortgages. But when I got the lender’s owner on the phone, he said, “Look Matt, no one wants the FBI digging through their files.” They had already sold the bulk of the loans to HSBC (Household Savings Bank Corporation).

Ethically, Pinnacle should’ve notified Household about the fraud. Instead, they sold HSBC the remaining loans and told me to keep the business coming. My company was doing about a million a month with them and the owner said, “It would be a shame to ruin our relationship over a few million in bad mortgages.”

ACCORDING TO THE FBI, mortgage fraud was reaching epidemic proportions by 2001 and Florida was leading the nation. Brokers were getting indicted all the time and inevitably people cooperate. That’s how I got busted the first time. Two brokers, Peter and Gretchen Zayas, were under investigation by the FBI for their participation in a “straw man scam.” They were indicted and immediately agreed to cooperate by setting me up.

We met at a pizzeria—both Peter and Gretchen were wired—and they got me to implicate myself in bank fraud. I was subsequently indicted for wire fraud.

At my sentencing, the judge lectured me about “ripping off retirees savings accounts and pension funds,” none of which I’d done. My parents were in the courtroom, the look on my father’s face was a combination of disappointment and disgust.

With the felony came 42 months of federal probation, the loss of my brokerage license, my income and a divorce. However, the felony only increased my illegal activities. I could’ve walked away. I should’ve walked away, but I didn’t want to get a job where I’d be asking people, “Would you like fries with that?” I didn’t want to be, what my father would’ve considered a “dead beat” or a “failure.” A felony didn’t change that.

I was plugged into everything from title agencies to the credit bureaus. I knew Fannie Mae and Freddie Mac guidelines better than most underwriters and I was familiar with the standard quality control procedures of the entire industry. I dated the manager of a Lawyer’s Title Agency for a few months and it turned into a crash course on public records. She taught me how to falsify Satisfaction of Mortgages and manipulate sales prices. I’d already discovered how to simulate nonexistent borrowers—with verifiable credit histories and 700 plus credit scores. In commemoration of Quentin Tarantino’s movie, Reservoir Dogs, I named my phantom borrowers: Lee Black, Michael White, Brandon Green and William Blue, among others.

Clearly something’s not right with me. It took me all of two minutes to figure out how to manufacture fake ID’s—using a laptop and transparencies—but I can’t find my car when I leave the mall.

“COX WAS VERY PROLIFIC in his mortgage fraud,” said Assistant U.S. Attorney McKenzie. “He created phony companies to supply fake pay stubs and income tax statements for straw borrowers that he employed or invented out of thin air. He put a different twist on the classic property flip.”

I created banks—complete with monthly statements, cancelled checks, 800-numbers and interactive websites. I’d clone SunTrust Bank’s website and make a few minor modifications, rename them: Bank of Ybor, Southern Exchange Bank of Clarksville, etc. I’d then use them to verify plump bank accounts, certificates of deposit and employment for my phantom borrowers.

The bank websites were so convincing that when the Secret Service agents eventually questioned me, they accused me of hiding almost $200,000 in Southern Exchange. The agents couldn’t understand why the bank wasn’t returning their messages or responding to subpoenas. When I explained that the bank didn’t exist, they seemed a little embarrassed.

My associates and I began purchasing inexpensive properties and recording the Warranty Deeds at three and four times their true sales price. I’d buy four or five houses using a phantom’s name, then borrow a million dollars against the properties using the inflated value. Then I’d make a few payments and let the loans slip into foreclosure.

When the banks’ collection agents started calling, I’d mail out a letter from a nonexistent relative—accompanied by an article on a recent Interstate pile-up—claiming the borrower had been in a catastrophic accident and the letters stopped. An investigator from one lender told The St. Petersburg Times, “It was impossible to determine if Green was ‘living or dead.’ His address was a UPS box, his phone a prepaid cell, his employer an answering service.”

By late 2003, my associates and I had inflated the value of over 100 properties and borrowed $11.5 million in fraudulent mortgages. The median value in Tampa’s Ybor City area skyrocketed. After examining 2003 sales prices from the nation’s largest metropolitan areas, Forbes.com listed Ybor City as one of the top 20 fastest appraising zip codes in the country.

THE SCHEME NETTED MILLIONS, but there were hiccups. At one point South Star Bank stumbled across my ruse. They verified a phantom borrower’s W-2 and discovered he’d never filed taxes. They also confirmed that his Florida ID number had never been issued and learned his social security number belonged to a toddler. The situation was deteriorating fast, so I contacted the bank and ended up on speaker phone with their head of security and several executives. I’ll never forget when he said, “When the FBI finds out who you are, and they will, you’re looking at spending a considerable amount of time in an eight-by-ten-foot concrete box!”

There was blood in the water, and South Star was in a frenzy. However, during the head of security’s rant I’d picked up on a discrepancy and exploited it. South Star was under the impression their $117,000 loan was secured by a $139,000 piece of property in average condition. In fact, it was attached to a $30,000 crack house. Had South Star foreclosed, they would’ve incurred a loss of roughly $100,000. Their attitudes changed pretty quickly when I pointed out how under-collateralized they were.

“What we need to be discussing is our mutual problem,” I said, “getting South Star’s money back.” Their primary responsibility was safeguarding South Star’s interests.

“When the FBI get’s a hold of you,” snarled one of South Star’s executives, “well get our money back.”

“Not true,” I replied calmly. “I’m a ghost.” I then explained that the money had been placed in several accounts opened using false identities and had since been withdrawn. “Assuming the FBI can catch me—which is doubtful—the likelihood of you recovering the funds is slim.”

After a little cajoling, South Star agreed not to contact the FBI, if I immediately returned the balance of the loan. Which I gladly did.

South Star wasn’t the only lender I was forced to repay. It got to be routine. If a lender stumbled across the scheme, they’d threaten to call the authorities, and in turn, I’d return their money.

It all started unraveling when my girlfriend and co-conspirator at the time, Alison Arnold, attempted to borrow close to $400,000 using a stolen identity. Barbara Byliski, the manager of Land American Title, suspected something was wrong at the closing. “The woman didn’t look like her ID and all she cared about was when she was getting her money,” said Byliski during an interview with The Times.

She began making calls and discovered the scam. The title company’s check was red-flagged and weeks later, while withdrawing the fraudulent funds, a second associate, Travis Hayes, was arrested by the Altamonte Springs Police Department inside Crown Bank. To avoid a stiff sentence, Hayes began secretly cooperating with the authorities. A joint state and federal taskforce was formed and subpoenas were issued.

I received a call from the title manager I’d once dated and from a lender’s sales rep—both warned me about the subpoenas. My associates were receiving calls from a St. Petersburg Times reporter regarding phantom borrowers and inflated sales. Days before an FBI raid and my inevitable arrest, I was tipped off by a friend—a Hillsborough County Sheriff’s Deputy. I was already on federal probation, so a lengthy federal prison sentence seemed inevitable. It wasn’t something I was planning on sticking around for.

I fled the state with my girlfriend, Rebecca Hauck. She was a blond P!nk look-a-like. We’d been dating just over a month. “When we left Tampa,” said Becky during a interview with Dateline, “I knew we were going to get involved in crime.” Becky was already fleeing trouble when she met me on Match.com. She was twice divorced and bankrupt by the age of 30. She had been banished to Florida by her Las Vegas employer for embezzling funds to cover her gambling debts. “Matt Cox seemed like the answer to my prayers,” she said. “He drove this great Audi TT. He had a fabulous Mediterranean-style triplex apartment.” The walls of my house were adorned with art deco murals. “What drew me to him was his artwork. When we met, I found him very funny, very charming.”

Despite my objections, Becky placed her 13-year-old son on a plane to live with his father in Las Vegas and joined me. Letting her was a huge mistake. We barely knew each other. Her behavior was erratic. Becky suffered from bipolar disorder and she refused to take her Zoloft. Between her mood swings and recreational drug habit, her behavior was unpredictable.

THE HUNT WAS ON. Special Agent Candace Calderon of the FBI, and half a dozen other agents raided my office three days after Becky and I fled Tampa. My passport, license and credit cards were flagged immediately; and a federal warrant was issued for my arrest.

On December 14, 2003, The St. Petersburg Times ran an article called Dubious Deals, exposing me as the mastermind behind a multi-million dollar mortgage scheme designed to bilk Tampa Bay banks out of

millions. Within weeks, more articles appeared: Target Of Land Inquiry Is Fugitive and Serial Mortgage Signer Sought. Dozens more followed.

IN ATLANTA, GEORGIA, we leased a luxurious downtown apartment, purchased expensive vehicles and acquired new names. Stealing identities is relatively easy. I ran an ad in the newspaper that read, Home Loans Available—Good/Bad Credit/No Problem. The phone never stopped ringing. If you sound confident and knowledgeable, people will give you everything you ask them for—even over the phone.

Becky and I used callers’ personal information to order their birth certificates, social security cards, driving records and voter’s registration cards. Using the information, we acquired state drivers’ licenses and passports from the U.S. State Department. It turned out to be easier and safer to obtain credentials through the states and federal government than it was to counterfeit them.

According to Louis B Schlesinger, Professor of Forensic Psychology at John Jay College of Criminal Justice in New York, “Master con men like Cox are charming, manipulative, cunning. They have an amiable façade, which makes them very adept at getting others to like them.”

There had never been any doubt how we intended to finance our lifestyle. We needed money and the quickest way to get it was to assume the identity of a home owner.

Becky leased a house in Alpharetta, Georgia, from a CPA named Michael Shanahan. I forged a Satisfaction of Mortgage releasing Shanahan’s Bank of America lien in public records. Then, as Shanahan, I borrowed multiple loans from local lenders totaling roughly $400,000.

John Holman, owner of Fieldstone Investments, later told The Atlanta Journal-Constitution, “Cox had three forms of identification, and a house that appraised at $190,000 and wanted to borrow $105,000 against it. It’s what you call a no-brainer [however,] it turns out this fellow didn’t even own the house.” Holman’s company received the balance of its mortgage from title insurance. But I walked away with over $100,000 of Fieldstone’s funds.

Using a dozen fake or stolen ID’s, Becky and I cashed the $400,000 in fraudulent mortgage loan proceeds in Atlanta. SunTrust Bank was the only institution to suspect something wasn’t right. While cashing a $29,000 check from one of Shanahan’s closings—issued to Scott Cugno, a stolen identity—the bank’s manager disappeared into the back room to verify the funds. I was pretty nervous at that point. Becky was calling me every three minutes screaming, “Get outta the bank!”

“I’m not leaving without that money,” I hissed. Everything I’d given the manager should’ve checked out in their system. It was all genuine. “Fuck this guy.”

The manager kept coming out of the back room to ask questions, while Becky was blowing up my cell, pleading with me to get out of the bank. Leave. Run. I finally asked the manager what was taking so long and he replied, “We’re trying to contact Mr. Shanahan…” My stomach dropped—the real Shanahan was listed in the local directory. Despite the urge to run screaming from the bank, I maintained my composure. “It shouldn’t be much longer, Mr. Cugno.”

But SunTrust didn’t call information, they called the title company that had issued the check; and the title company gave them Shanahan’s number—my cell number.

I was sitting in the bank manager’s office when SunTrust called to verify the check. A female asked to speak with Mr. Shanahan and I said, “This is Michael Shanahan . . .” She asked me to verify the amount of the check and the payee. “No problem.”

A minute later, the bank manager counted out $29,000 in cash on his desk and I walked out of the bank.

Shanahan discovered his identity had been hijacked in late June 2004. By the time Coweta County Sheriff’s deputies arrived at the home, we had vanished. Due to the identity theft and the counterfeit documents, Agent Andrea Peacock, of the U.S. Secret Service was notified. She later told the press, “We had no idea where they were.”

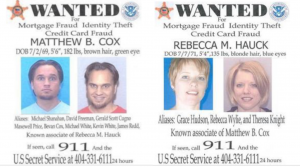

John and Jane Doe warrants were issued. Wanted posters with our photos were distributed to title companies, banks and lenders throughout the southern states. Atlanta’s WXIA News reported, “With ‘John and Jane Doe’ out there, no homeowner is safe.” Our faces were everywhere. I hadn’t expected Secret Service involvement. Unlike the FBI, they were actively searching for us. Agent Peacock quickly discovered our true identities and I was placed on the Secret Service’s most wanted fugitive list.

Cosmetic surgery seemed like a reasonable solution to the ever-increasing media attention. Becky got breast implants and lipo-suction. I underwent rhinoplasty, lipo-suction, a mini face-lift and hair grafts. My teeth were capped and whitened. The surgeries were painful, but not nearly as painful as federal prison.

WE WERE ON VACATION in New Orleans, when the U.S. Marshals got a tip that Becky and I were in the area. The Marshals dispatched several agents to the French Quarter, but the federal agents couldn’t locate us in the crowds.

Our hotel was only blocks away from where the Marshals’ tipster indicated we’d be. For all I know, we passed them on Bourbon Street. We weren’t looking for federal agents, we were taking tours, visiting museums and shops.

Becky and I vacationed in the Caribbean, partied in Mexico and gambled in Vegas. She later told Fortune magazine, “I had diamonds. I had a Rolex. He’d just give me cash for whatever I wanted . . . I drove an Infiniti. Great clothes, makeup, nails. I had everything.”

It was an expensive and stressful lifestyle. We had to stay ahead of the FBI, the Secret Service and the Marshals. After each scam, we’d abandon our vehicles in international airports long-term parking, leaving clues for the federal authorities that led nowhere—blind alleys. I’d wedge a Madrid hotel brochure in the front seat, stick some Euros in the glove box, or leave the book Spanish for Dummies in the truck.

Weeks or months later, Becky and I would read in amazement when the media reported the fugitives were believed to be in Spain or France.

ASSISTANT U.S. ATTORNEY McKenzie later said, “Throughout these schemes, Mr. Cox is taunting law enforcement . . . Like the time he signed a forged document using the name C. Montgomery Burns, the aging tycoon in The Simpsons.” My childish antics eventually earned me the top spot on the Secret Service’s most wanted fugitive list.

We were so brazen that the media dubbed us, “The Bonnie and Clyde of Mortgage Fraud.” The Chicago Tribune ran a three part series titled, The Fugitive, chronicling our exploits. “He’s the ‘poster child’ for identity theft,” said McKenzie. “He treated fraud like a game.”

When we needed clean identities, I’d tote a Salvation Army ID badge on my belt and survey the homeless. When we needed fresh social security numbers, I’d forge birth certificates for nonexistent babies—along with immunization records. I’d tell the Social Security Administration my son or daughter was born at home with a midwife and had never received a social security number. They’d immediately issued me a brand new number. I’d then combine the genuine documents to acquire state ID’s, credit cards, bank accounts and of course, real estate.

IN COLUMBIA, SOUTH CAROLINA, using the name of a Las Vegas transient, Gary Sullivan, I convinced sellers to owner-finance their properties. I then cleaned the titles of liens and borrowed $1.3 million in fraudulent mortgages. “In our case,” said Dr. Bruce Brown, one of the South Carolinian sellers, “Cox closed on six loans [totaling over $800,000] in the span of a few days.”

“He talked a great game,” said Mary Nell Degenhart, a Columbia lawyer who handled a loan closing for Sullivan. “He made you feel like you were dealing with a pro. He had all the right documentation, all in perfect order. Although in retrospect, all fake.” But this time I slipped up and applied for a loan with BB&T Bank, a week before the loan officer went on vacation. The title search ended up being ordered a week after I’d closed the bulk of Sullivan’s loans. By the time the title abstractor got to the courthouse, multiple mortgages had been recorded in public records. “It was outright illegal,” said Degenhart.

The FBI was notified and Columbia banks were alerted. I was nabbed by the Richland County Sheriff’s Deputies at Wachovia Bank. I thought, This is it. They had the Secret Service’s most wanted fugitive in handcuffs. But when the Columbia investigator got on the phone with the head of Wachovia’s fraud department, their “fraud guy,” kept referring to me as “Mr. Sullivan.” No one seemed to know who I was. Wachovia knew Sullivan had swindled several banks, but they hadn’t quite put all the pieces together.

“They’re saying you’ve got three first mortgages,” asked the investigator holding the receiver slightly away from his ear. “Is that true?” It wasn’t. I actually had seven: two satisfied mortgages, four new mortgages and one shell mortgage—that didn’t include the multiple mortgages I’d taken out on a second property across town—all were first mortgages.

“Yes and no.” I explained I had a first mortgage with Wachovia, a second with Fieldstone Mortgage and a credit line with SunTrust Bank—which made sense, but was absolutely untrue. Here’s the thing, way more fraud is committed by loan officers and brokers than borrowers, so I decided to muddy the waters. I gave the investigator my Golly Gee Wiz expression and suggested, “the loan officers might’ve done something illegal, but not me.”

Wachovia’s department head insisted all three mortgages were in first position. “He’s saying they haven’t committed fraud, you have . . . and he wants you arrested.” Yikes!

“Which explanation sounds more reasonable,” I shot back, “a guy with no financial experience fooled a bunch of banks into lending him half a million dollars (it was actually $1.3 million) or several experienced loan officers bent the rules to make a fat commission?”

I could hear Wachovia’s fraud guy screaming something about identity fraud. The investigator glanced at my South Carolina Identification card and responded, “No, it’s valid. I pulled Mr. Sullivan’s information myself. It’s him—”

I leaned into the detective and whispered, “Now I’m not even Gary Sullivan? Come on . . .” With the head of Wachovia’s fraud department yelling to arrest Sullivan for bank fraud, I convinced the investigator there was a problem, but it was at the bank, and he released me. He then asked me to follow him to the Columbia Police Department to fill out an incident report.

On the way out of the bank one of the deputies noted I was much shorter than the five-foot ten-inches posted on Sullivan’s Nevada driving record. “Well,” I shrugged, “with a good pair of shoes.” The three law enforcement officers burst into laughter.

On my way to the police department, Becky called. She was screaming, “Get on the Interstate and run.” I told her, “The worst that’ll happen is I’ll be arrested as Gary Sullivan,” a scenario we had been over a dozen times. If I was ever arrested Becky was to immediately hire an attorney to get me out on bond—before the authorities cross-referenced my fingerprint through AFIS (Automated Fingerprint Identification System). Unless your identity is in question, it could be weeks before the local cops run your prints. And I had more Sullivan identification on me than the genuine Sullivan. But Becky refused. “If you go into the police station and get arrested, I’m not getting you out on bond!” she screamed. “I’m not gonna risk everything I’ve got—you need to get outta Columbia, now!” But I went in anyway.

Inside the station, I answered some questions and signed a statement. I stood a few feet away from a wall full of wanted posters—including my own full color Secret Service wanted poster—but no one seemed to notice. When the investigator eventually released me, I went straight to another bank and withdrew funds. Then another. Eventually I headed to Houston, Texas, where Becky had rented a plush new apartment downtown.

“It was unbelievable,” said Degenhart. “Cox had the police laughing at his jokes. He charmed them . . . This whole scam is the talk of the real estate community. It just amazes me he got away with it.”

The FBI and the Secret Service quickly put the South Carolina scam together with my modus operandi. They began tracking leads: UPS Boxes, Tracfones and answering services, all but one were blind alleys. The Columbia investigator had taken down my tag number. Which was registered to an alias’ address in Charlotte, North Carolina.

Becky and I rendezvoused in Houston. We argued. She was off her meds and I couldn’t deal with it anymore. So, I left her; and I feel bad about that, but she didn’t have a problem ditching me in Columbia. I left her with roughly half a million dollars in cash and headed to North Carolina. My only identification was in the name of a known alias and my only vehicle was 700 miles away in Charlotte.

One year later, Becky was arrested—after confiding her location to a family member—by the Secret Service in Houston.

On my way to North Carolina, I stopped and bought a Virgin Mobile prepaid cell and phoned my mother in Tampa. I wanted to hear her voice. To hear her tell me everything was going to be alright. She wanted to see me, but she also told me she knew it was too dangerous. I could hear my father yelling in the background. She told me, “I love you and to be safe.”

Then I called a broker that used to work for me; she pled with me to contact the FBI. “Just hear what they have to say. Maybe you could turn yourself in.”

Agent Calderon had a personality bred out of a position of authority and contempt for those she deemed inferior—I’m certain I fell into the inferior category. She was unprofessional and rude. Combative. She told me they were going to catch me. They were close. “We’re going to find you.”

“So, what’s taking you so long.”

“We’re ninety percent sure of where you’re at,” she snapped, and I shot back, “Only one hundred percent counts.”

Once she cooled off, the agent began negotiating between the U.S. Attorney’s Office in Tampa and me. After several calls, it seemed like we were making progress. What I didn’t know, was that Calderon had contacted the Marshals and they had tracked my prepaid cell. At that moment they were racing toward my location.

After several calls, Calderon began to break down my resolve. She talked about my aging parents and my son. She had almost convinced me to surrender in exchange for a seven year plea deal, when I caught the agent in a lie. Despite my specific request for an all-inclusive deal, Calderon had never even called the U.S. Attorney’s Office in Atlanta. It was all bullshit. The Tampa FBI wanted to grab me before the Atlanta Secret Service did. It was all a con game. I told the agent, “I wouldn’t believe you if you said water was wet,” and I slung my prepaid cell out the window as the Marshals’ sedan raced by my vehicle.

There was no going home.

“It seems to me,” said Assistant U.S. Attorney McKenzie, “Cox was teasing and taunting the FBI agent . . . [H]e has no respect for the law.”

ON MARCH 11, 2005, I stepped into a Charlotte, North Carolina, Starbucks—less than a block away from my downtown apartment—as two employees from my apartment building were picking up an order. They recognized me and were instantly rattled. A frantic conversation ensued between the pair. Seconds later the female leasing agent darted out of the café, leaving her co-worker holding a tray full of coffee.

It never occurred to me that two federal agents were at that very moment a block away interviewing the staff of my apartment building. A minute later the female apartment complex employee burst into the leasing office—startling the Marshals—and gasped, “He’s at the Starbucks!”

The two Marshals bolted out of the office and shot down the street toward the café, pushing pedestrians out of their way.

I’m just not that bright sometimes. I didn’t put it together until I got into my Infiniti G35 and the guy from the apartment complex dropped his tray of lattes and started screaming, “He’s right here! He’s right here!”

I swiveled around and two men in gray suits were running full throttle toward the back of my vehicle. I slammed down the accelerator, roared away from the curb and disappeared down the city street, leaving the two agents behind. That’s when I put it together. And the media was calling me a “mastermind.”

“EACH TIME THE AUTHORITIES tightened their noose, Cox managed to slip away,” said the assistant U.S. attorney. “Mr. Cox was able to elude the U.S. Marshals, the FBI and the Secret Service for year . . . it was fun for him.”

I got lucky a lot. Once, while passing through airport security I was selected for a random screening. While digging through my carry-on, the security officer found an Alabama ID in a CD case—in a second alias’ name. The security officer was calling me Mr. Carter—the name on my ticket. Yet, she was staring at the ID card she’d just found in the name of Jeffery Gilbert. I couldn’t have been more screwed.

“Mr. Carter,” she asked, “why was this in a CD case?” I responded, “Was it? I’ve been looking for that for months,” and I quickly slipped the ID out of her hand, before she had a chance to read the name.

WITHIN WEEKS OF THE NEAR miss in Charlotte, I had ID’s in several new names and a posh new apartment off Music Row in Nashville, Tennessee. By the end of the month, I had abandoned one vehicle at North Carolina’s Charlotte International Airport and purchased another one. And I continued to commit fraud.

In September 2005, Bloomberg Businessweek ran an article called, Sharks In The Housing Pool featuring Becky’s and my escapades along with our wanted posters. There wasn’t a financial institution in the country that didn’t subscribe to that magazine. My photo was everywhere. I was in the middle of running multiple scams in multiple names and Businessweek was calling me a shark.

I was seriously concerned about the exposure—when you’re watching Jaws no one’s rooting for the fish—but the article didn’t deter me. I just couldn’t stop. There’s something intoxicating about having a Wells Fargo or SunTrust Bank loan officer tell you, “You’ve been one of the best customers I’ve ever worked with.” Then hand you a $200,000 check and thank you for swindling their bank.

“With Cox it wasn’t about making money, it was the thrill of the bluff,” said Michael Markham, a Tampa real estate attorney, during an interview with the Times. “He recognized the weaknesses in the real estate system and figured out how to profit from them.”

In Nashville, I faked an urban renewal program by building a website, NashvilleRestorationProject.com, which boasted that Nashville’s JC Napier housing project was scheduled to be torn down, and the surrounding area had been designated by the city’s Future Comprehensive Plan as a future historic district. Sounded good. I then purchased over 20 dilapidated properties in the Napier subdivision and recorded the sales at five times their true value. Values jumped from $40,000 to over $200,000 in six months.

At that point, it was simply a matter of acquiring licensed appraisal software and creating dozens of counterfeit appraisals. The banks couldn’t lend my fake borrowers money fast enough—Bank of America, JP Morgan Chase, Wells Fargo and First Tennessee Bank. I borrowed over $2.7 million from Nashville lenders. I got Countrywide for just over $600,000. I could’ve left the country at that point, but I didn’t.

About the same time I should’ve been packing my bags, I met Amanda Gardner on YahooPersonals.com. She was a 25-year-old veteran of the Iraq war. You can’t imagine how amazing some of the women on these dating sites are. Amanda was that kind of amazing. She was a vivacious brunette with Mediterranean features, fresh out of the Army and looking for adventure. Amanda was up for anything; from my fugitive status to trysts with other women—our favorite sexual partner was Trina Taylor, a 29-year-old athletic blonde I’d dated when I first got to Nashville.

“He was wonderful to me,” said Amanda, during an interview with the Times. She was captivated by my art deco murals which decorated my fashionably renovated Nashville bungalow. “He was an artist. He’d written books.” I provided a sumptuous lifestyle for us; exotic vacations, luxury vehicles and expensive jewelry. “He did everything he could to make me feel one hundred percent special.”

During a vacation in Venice, Italy, we visited the famous Bridge of Sighs, which got its name from the sighs of the condemned prisoners who received their last view of daylight and freedom from the bridge’s tracery windows. I’d pushed incarceration out of my mind for nearly three years, suddenly, I couldn’t think of anything else.

I must have looked horrible, because Amanda leaned into my ear and whispered, “It’s not going to happen.” But she didn’t know that. I didn’t know that. The biggest mistake I could have made was letting someone know who I was, and I’d already done that.

That bridge was an omen.

IN NOVEMBER 2006, Fortune magazine ran an article titled, The Bonnie and Clyde of Mortgage Fraud, covering Becky’s arrest and life on the run. It was an absolutely distorted account of our relationship. She described me as controlling and abusive. Armed and dangerous. The truth is, I never had a weapon and the only danger I’d ever posed was to financial institutions.

As damning as the Fortune article was, Amanda and I felt the effect was negligible. However, when Amanda came across a blog discussing an up and coming April 2007, Dateline NBC episode on me, titled The Thief of Hearts, focusing on my mortgage schemes and the trail of broken hearts I’d left behind, it was time to leave the States. Permanently. My face was going to be in living rooms across the nation. They had Alison Arnold and Becky saying I’d forced them to commit bank fraud, get breast implants and leave their kids. They were out and out lies orchestrated by their lawyer, Paula Hutchinson, from the Johnny Cochran law firm. However, by now, I knew the media was more interested in a good story than the truth.

Amanda and I began removing cash from my numerous Nashville bank accounts and researching Australia’s policy on foreign nationals. I had a passport in a vagrant’s name. He didn’t have a criminal record, so permanent residency wasn’t going to be a problem.

What I didn’t know, was Amanda had confided my fugitive status to our sexual liaison, Taylor, not realizing that our girlfriend would contact the Secret Service to collect on my reward. It’s my understanding she got $10,000. Funny thing is, I would have given her a million dollars for a ten minute head start.

On November 16, 2006, after a three day surveillance operation, six Secret Service agents swooped in barking, “Get on the ground! Get on the ground!” They slammed me to the pavement in front of my Nashville bungalow and arrested me. But after all the plastic surgery, even the agents could barely recognize me.

“You think it’s him?” one agent asked the lead agent.

“It’s him,” he replied. “Look at his eyes. It’s him.”

After being flown to Atlanta, my Federal Public Defender, Millie Dunn, convinced me to be interviewed by the Secret Service, the FBI and the U.S. Attorney’s Office. “It’s that or you spend the next fifty-four years in federal prison.”

For seven days the agents bombarded me with questions regarding my scams and how I’d pulled them off. I was amazed at how little they knew. These were the premier law enforcement agencies in the country and they’d had virtually no training or experience in the most basic real estate fraud schemes.

Regardless of my cooperation, a year later, Assistant U.S. Attorney McKenzie vilified me in a courtroom full of reporters. “We need a substantial sentence to reflect the seriousness of the offense,” she croaked to U.S. District Judge Timothy Batten, Sr. “Most importantly, to protect the public from further crimes of the defendant.”

The judge agreed. “The degree of consciousness and forethought used to accomplish these schemes was stunning,” he said, “It required a commitment level that reflects a sociopathic disregard…or something else that is profoundly wrong,” and he sentenced me to 26 years and four months in prison—one of the harshest mortgage fraud related sentences in history.

It was crushing, and yeah, I cried like a baby. My mother cried. Hell, my lawyer cried.

As Assistant U.S. Attorney McKenzie left the courtroom she was surrounded by reporters requesting a quote. “Mr. Cox may have written the book on fraud,” she said, “but we wrote the last chapter.”

THE MEDIUM SECURITY PRISON, at the Federal Correctional Complex in Coleman, Florida, is constructed of concrete and steel. Encircled by motion sensitive chain link fences topped with razor wire. There are gangs. Fights and riots. The day I got there, someone was stabbed on the recreation yard. I remember thinking, This is not a good environment.

Roughly, a year later, my father came to see me. It was the first and only time he’d come to see me alone. We sat across from each other in Coleman’s visitation room, awkwardly trying to connect. Since childhood, I’d craved love and respect from a man who had never seemed inclined to give either. But that day was different. “The things you’ve done are amazing,” he chuckled. “You’ve lived an incredible life, Matthew… I’m not proud of where you ended up, but I’m proud of you.”

“Dad, I’ve got twenty-six years,” I said. “I’m finished.”

He shook his head. “No, you’re smart and you’re clever. You’ll get out of this. This isn’t it for you.”

Shortly after my father left, I contacted my attorney. With the help of the U.S. Attorney’s Office and the District Court, over the next several years, I participated in an interview with Dateline NBC and CNBC’s American Greed; several articles for the Scotsman Guide—a mortgage industry magazine—and The St. Petersburg Times.

“The scope, complexity and nefariousness of Cox’s fraud are breathtaking,” wrote Judge Batten; in a letter to the Warden requesting his assistance in obtaining an on-camera-interview with me for the National Mortgage Loan Originator School. “Consequently, Cox’s cooperation with the government in exchange for a reduced sentence is an important part of his case.”

In 2012, I was interviewed and helped write an Ethics and Fraud course which is used as part of the federal government’s continuing education requirements for the nation’s mortgage brokers. In addition, I wrote a federal Red Flags Rules course which is used to teach financial officers techniques to detect fraud and prevent identity theft.

My father died on April 18, 2013, days after I’d received notice the U.S. Attorney’s Office filed a motion to reduce my sentence. Months later, I was taken back to court and my sentence was reduced from 26 years and four months to 19 years and six months. With time off for good behavior and some programming, I’ll be released in 2022. But I’m still working to reduce my sentence. My father was right, this isn’t it for me. This isn’t my last chapter.